For anyone marketing property in the UAE, this is a valuable report – Pulled together in a matter of minutes by Google Gemini, demonstrating the power of AI. It covers the key Emirates of Dubai, Abu Dhabi and Sharjah, we will focus on the smaller Emrates in future posts.

Snapshot of UAE Property Market Trends: 2025 Outlook

1. Executive Summary

The UAE property market is demonstrating remarkable resilience and robust growth in 2025, underpinned by strong economic fundamentals, strategic government initiatives, and significant international investor confidence. This report provides a concise overview of key trends, market dimensions, and crucial price band segmentation across the major emirates.

The market’s expansion is evident across the board, with Dubai and Abu Dhabi leading in transaction volumes and values. A notable characteristic of the current market is the dominance of the ultra-luxury and high-value property segments, which are experiencing exponential growth, largely fueled by the continuous inflow of High-Net-Worth Individuals (HNWIs) and Ultra-High-Net-Worth Individuals (UHNWIs). Concurrently, the rental market remains exceptionally strong, with attractive yields and continued upward pressure on prices for both short-term and long-term leases.

Despite the overall positive trajectory, an affordability gap persists, particularly for mid-income earners, underscoring the ongoing need for diversified housing solutions. The market’s sustained momentum is fundamentally supported by strategic drivers such as consistent population growth, the appeal of Golden Visas, and proactive government urban development plans.

The market’s evolution points to divergent growth patterns across the emirates, signaling a more mature environment in Dubai and Abu Dhabi. Growth in these emirates is increasingly concentrated in specific luxury and high-yield areas, rather than uniform expansion across all segments. This indicates a market that has moved beyond pure speculative growth, driven instead by end-user demand for premium properties and strategic investment for yield. Sharjah, while also experiencing significant growth, is leveraging legislative reforms to attract a broader investor base, suggesting it is in a different phase of market development. This divergence necessitates a nuanced, emirate-specific investment strategy, as a generalized approach based on overall UAE trends could lead to missed opportunities or misinterpretations of market risks. It also implies that government policies are becoming increasingly tailored to the specific market needs and maturity levels within each emirate.

2. Overall Market Performance & Economic Context

Key Economic Indicators & GDP Forecasts (2024-2025)

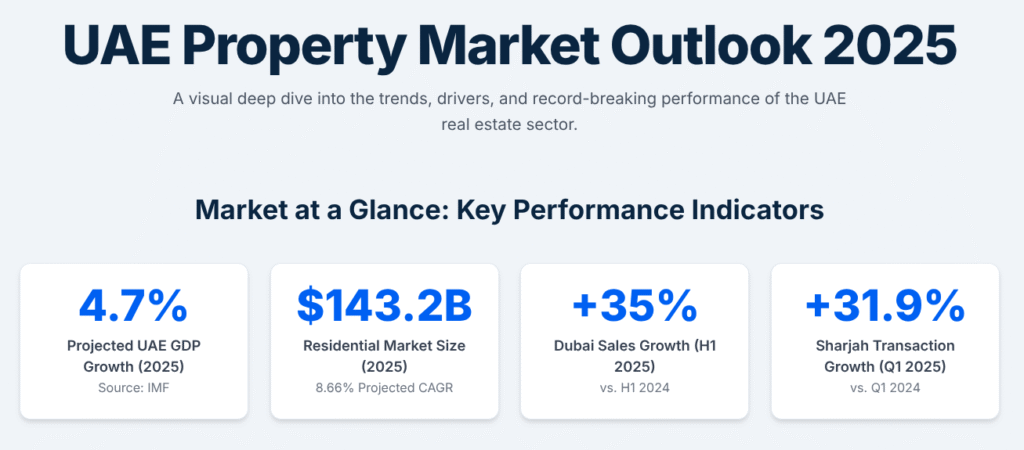

The UAE economy is projected for robust growth, with its Gross Domestic Product (GDP) forecasted to reach 4.7% in 2025, an increase from 3.8% in 2024. This growth is particularly significant given the prevailing global macro uncertainty and ongoing trade tensions, which have led to a more cautious global growth outlook from institutions like the IMF. The non-oil private sector remains the primary engine of this economic growth, demonstrating resilience despite potential negative effects on global trade from higher tariffs. The International Monetary Fund (IMF) anticipates the UAE economy to expand by an annual average of 5% in 2025, while the World Bank offers a more conservative forecast of 4.1% annual growth over the next two years. Headline inflation within the UAE remains comparatively low, forecasted at 2.5% in 2025 (up from 2.1% in 2024), generally staying within historical norms despite continued growth in housing costs.

This economic resilience acts as a fundamental stabilizer for the real estate market. The strong performance of the non-oil private sector and the government’s ongoing economic diversification efforts are crucial factors. This suggests a decoupling of the real estate market’s health from traditional oil price volatility, indicating a maturing and robust economy. The real estate sector’s substantial contribution to Dubai’s GDP, estimated between 5-7% , further solidifies its role as a core economic pillar, rather than merely a beneficiary of hydrocarbon revenues. This resilience enhances investor confidence, particularly for long-term commitments, as the market appears less susceptible to commodity price swings. It also implies that government policy will continue to prioritize non-oil sector growth, which indirectly supports real estate through job creation and population influx.

UAE Real Estate Market Size & Growth Forecast (2024-2033)

The total UAE real estate market size reached USD 36.92 billion in 2024. Projections indicate it will grow to USD 49.96 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 3.07% during the 2025-2033 period. Focusing specifically on the residential real estate market, its value is estimated at USD 143.22 billion in 2025 and is forecast to climb to USD 217.09 billion by 2030, advancing at an impressive 8.66% CAGR. This highlights a strong focus and accelerated growth within the residential segment.

Dubai’s real estate sector alone recorded AED 761 billion (approximately USD 207.2 billion) in transactions in 2024, representing a 20% rise in value year-on-year and a 36% growth in volume. This underscores Dubai’s significant contribution to the overall UAE market. In the first half of 2025, Dubai’s real estate market completed AED 260 billion (USD 70.8 billion) worth of sales transactions, marking a substantial 35% increase compared to the same period in 2024.8 By March 2025 (Q1), Dubai’s total sales reached AED 142.7 billion, signifying the fastest pace in the city’s history.9

It is important to note the varying figures reported for market size, which can be attributed to different methodologies or scopes. For instance, the USD 36.92 billion figure for the “UAE real estate market size” likely represents a specific segment or a more conservative valuation, possibly excluding land or certain commercial transactions, or perhaps it is a valuation of market activity rather than total asset value. In contrast, the USD 143.22 billion figure explicitly refers to the “UAE residential real estate market,” which is a subset of the overall market but still significantly larger.5 Dubai’s AED 761 billion (USD 207.2 billion) figure represents thetotal transaction value for just one emirate, encompassing both sales and rentals, and potentially commercial properties. This highlights the importance of clarifying the scope—whether it refers to the total market, residential, commercial, sales value, or total transaction value—when discussing market size. For stakeholders, this means that while the market is undeniably large and growing, precise comparisons require careful attention to the definitions and scopes used by different reporting agencies. This underscores the need for granular data and transparent reporting to avoid misinterpretation, especially for investment decisions, and indicates that the residential sector alone constitutes a massive component of the UAE’s real estate landscape.

Table 1: UAE Real Estate Market Size & Growth Forecast (2024-2033)

| Metric | Value (2024/2025) | Forecast (2030/2033) | CAGR (2025-2030/2033) | Source |

| Overall UAE Real Estate Market Size | USD 36.92 Billion (2024) | USD 49.96 Billion (2033) | 3.07% (2025-2033) | 1 |

| UAE Residential Real Estate Market Size | USD 143.22 Billion (2025) | USD 217.09 Billion (2030) | 8.66% (2025-2030) | 5 |

| Dubai Total Transaction Value | AED 761 Billion (2024) | – | – | 6 |

| Dubai H1 2025 Sales Transaction Value | AED 260 Billion (2025) | – | – | 8 |

| Dubai Q1 2025 Total Sales | AED 142.7 Billion (2025) | – | – | 9 |

3. Dubai Property Market: Trends & Price Segmentation

H1 2025 Transaction Volume & Value Highlights

Dubai’s real estate market demonstrated exceptional performance in the first half of 2025, recording AED 260 billion (USD 70.8 billion) worth of sales transactions. This represents a substantial 35% increase compared to the same period in 2024, highlighting sustained confidence in the city’s property market. The secondary market, comprising ready properties, significantly outpaced the off-plan segment, with its sales transaction value surging by 46% year-on-year, compared to a 25% increase in off-plan transactions. This indicates a clear shift in buyer demand towards ready, quality stock.

Demand for family homes was particularly strong, with villa and townhouse sales transaction value increasing by 55% in the first six months of 2025, compared to a 22% increase for apartments. While apartments still accounted for the majority of secondary market transactions by volume (78%), villas and townhouses made up a significant 22%. Mortgage activity also remained robust, with Dubai recording 11,014 mortgage transactions in Q1 2025, totaling AED 41.1 billion, reflecting continued investor confidence. Daily transaction volumes frequently exceeded AED 2 billion as recently as January 2025, serving as a strong indicator of active and optimistic buyers.7 Overall residential prices in Dubai saw a 20.7% year-on-year increase as of March 2024. Property prices across Dubai are projected to rise by 5-8% annually in 2025, with an average increase of 8% predicted across the overall residential market. As of mid-2025, the average price per square foot for properties in Dubai ranges between AED 1,100 to AED 1,400, contingent on location, property type, and project status (off-plan versus ready built).

Property Price Band Analysis: Luxury, Mid-Range, and Affordable Segments

The Dubai property market exhibits distinct trends across its price bands.

- Luxury Segment: This segment continues to be a significant driver of market value. The ultra-luxury segment, defined as properties above AED 10 million, recorded a staggering 113% increase in sales volume in H1 2025. This surge underscores growing investor confidence and the preference of HNWIs for Dubai as a destination for long-term capital growth. The AED 5 million to AED 10 million price bracket also experienced substantial growth, with a 50% increase in sales volume in H1 2025. Luxury properties are broadly expected to see a 5% average price increase in Dubai in 2025, with luxury villas, beachfront homes, and penthouses in prime areas like Dubai Hills Estate, Palm Jumeirah, and Jumeirah Golf Estates anticipated to witness even higher price increases of 8-10%. In 2023, sales of properties valued at AED 10 million and above nearly doubled to $7.6 billion. Furthermore, 2024 saw 948 luxury property sales (AED 15 million+), with Palm Jumeirah and Dubai Hills Estate leading in transaction volume. Developers are responding to this robust demand, with an additional 19,700 luxury properties slated for delivery in 2025. The astonishing growth in the ultra-luxury segment is not merely a segment trend but a significant driver of overall market value. It serves as a strong indicator of high-net-worth individual confidence in Dubai as a long-term investment and lifestyle destination. This segment’s performance reflects the city’s success in attracting global wealth, reinforcing its status as a secure and attractive hub for capital preservation and appreciation.

- Mid-Market Segment: This segment plays a crucial role in housing skilled expatriates, typically those earning AED 3,000–10,000 per month. Mid-market apartments are projected to experience 5-7% price growth in areas such as Jumeirah Village Circle (JVC) and Dubai Sports City. In 2024, the mid-market segment accounted for 47% of the UAE residential real estate market size.

- Affordable Segment: The term “affordable” in Dubai is relative, signifying more accessible prices compared to the ultra-luxury segments. Key areas offering more economical residential options include International City, Dubai Production City, Dubai Silicon Oasis, Jumeirah Village Circle (JVC), and specific sub-communities within Dubailand. These areas are generally more affordable due to factors such as a higher density of smaller units, greater distance from prime business districts, a focus on essential rather than luxury amenities, newer development, and a more suburban setting. Despite governmental efforts and new projects, only about 25% of new stock is genuinely accessible to average families, indicating a persistent affordability gap.

Secondary vs. Off-Plan Market Dynamics

In the first half of 2025, the secondary market significantly outpaced the off-plan segment. This trend is driven by a pronounced shift in buyer demand towards ready, quality stock and an ongoing shortage of available villas and townhouses. The sales transaction value in the secondary market surged by 46% year-on-year, whereas the off-plan segment saw a 25% increase. Similarly, average sales prices in the secondary market rose by 15%, while off-plan prices increased by just 5%.

This notable outperformance of the secondary market, particularly for villas and townhouses, coupled with higher price growth in this segment, points to a strong “flight to quality” and an immediate demand for ready, high-quality properties. This suggests that buyers, especially end-users and those seeking immediate returns, are willing to pay a premium for properties that are move-in ready and located in established communities. The scarcity of ready villas and townhouses is a key factor driving up prices in the secondary market. While off-plan properties continue to offer future capital appreciation potential, the immediate market value is clearly concentrated in existing, desirable properties. The narrowing of off-plan premiums as developers increase supply further supports this, indicating an adjustment to the market’s current appetite for ready units. This implies that the market is maturing beyond pure speculation on future projects, with a greater emphasis on tangible assets.

Rental Yields by Property Type & Key Areas

Rental prices in Dubai are forecasted to jump by 18% for short-term rentals and 13% for long-term leases in 2025, a trend driven by soaring demand and limited supply. Dubai’s average gross rental yields stood at 6.31% in Q2 2025.

Specific apartment rental yields in Q2 2025 vary significantly by area and unit type:

- Downtown: Studio 8.42%, 1-Bedroom 5.83%, 2-Bedroom 5.17%, 3-Bedroom 5.23%, 4+Bedroom 5.22%

- Palm Jumeirah: Studio 8.71%, 1-Bedroom 4.75%, 2-Bedroom 3.97%, 3-Bedroom 3.17%, 4+Bedroom 1.30%

- Dubai Marina: Studio 5.23%, 1-Bedroom 6.11%, 2-Bedroom 5.76%, 3-Bedroom 5.56%, 4+Bedroom 4.68%

- Business Bay: Studio 6.96%, 1-Bedroom 6.28%, 2-Bedroom 5.67%, 3-Bedroom 4.95%

- JLT: Studio 8.13%, 1-Bedroom 6.33%, 2-Bedroom 5.42%, 3-Bedroom 5.95%

- JVC: Studio 7.94%, 1-Bedroom 7.11%, 2-Bedroom 7.04%, 3-Bedroom 7.12%

- Arjan: Studio 8.20%, 1-Bedroom 6.96%, 2-Bedroom 7.06%

- Al Furjan: Studio 8.75%, 1-Bedroom 7.02%, 2-Bedroom 6.86%

Forecasted rental yields for 2025 by property type in Dubai indicate: Studios at 7.58%, 1-bedroom apartments at 6.96%, 2-bedroom apartments at 6.89%, and 3-bedroom apartments at 6.63%. Ready villa prices surged by 26% in 2024, reflecting a growing appetite for spacious, family-friendly living.

4. Abu Dhabi Property Market: Trends & Price Segmentation

Q1 2025 Market Performance

Abu Dhabi’s real estate market recorded steady and broad-based growth in Q1 2025, with gains observed across residential, office, retail, and hospitality segments. In the rental segment, average prices increased by 2.2% in Q1 and 9% year-on-year. The average annual asking rent for apartments in Abu Dhabi City reached AED 114,000. Studio apartments averaged AED 63,000, one-bedroom units AED 89,000, two-bedroom units AED 125,000, and three-bedroom units AED 180,000.

In terms of capital values, Saadiyat Island continued to lead Abu Dhabi’s villa market with an impressive 21.2% annual increase, significantly outpacing Al Raha (8.2%) and Mohammed Bin Zayed City (4.7%). More modest gains were seen in Al Reef (2%), while Hydra Village prices remained stable. For apartments, Al Reef showed strong annual gains of 7.5%, followed by Saadiyat Island (6.2%) and Al Muneera Island (5.7%). The office market remained resilient with high occupancy and rental growth, with asking prices climbing 6% in Q1 and rents in core commercial districts jumping 8% in Q1 and 31.8% year-on-year.

Property Price Band Analysis: Luxury and Affordable Segments

Abu Dhabi’s market also presents clear distinctions across luxury and affordable segments.

- Luxury Real Estate (Q1 2025):

- Luxury Apartments: Yas Island recorded an average selling price of AED 1.87 million, with a 2.54% quarterly increase, and the best Return on Investment (ROI) for luxury apartments at 6.99%.

- Luxury Villas: Yas Island led the luxury villa market with an average price of AED 4.68 million and an average annual rent of AED 229,000, showing a 1.33% increase. Saadiyat Island achieved the best ROI for luxury villas at 5.6%.

- Luxury Off-Plan Properties: Demand for luxury off-plan apartments was notable in Yas Bay (average price AED 2.02 million), Saadiyat Cultural District (AED 4.45 million), and Al Maryah Vista 2 (AED 1.11 million). For luxury off-plan villas, Yas Acres (AED 5.56 million), Saadiyat Lagoons (AED 8.98 million), and Al Jurf Gardens (AED 5.36 million) saw the largest demand.

- Affordable Real Estate (Q1 2025):

- Affordable Apartments: Al Reem Island had an average selling price of AED 1.54 million, with an ROI of 7.31%, and a 3.57% increase in price per square foot in the last quarter. Khalifa City was the top location for affordable apartment rentals, with an average annual rent of AED 44,000. Al Reef offered the best overall returns for apartments at 10.08%.

- Affordable Villas: Al Reef was the leading location for budget villas, with an average price of AED 2.21 million and an ROI of 6.23%. Mohammed Bin Zayed City was identified as the best area for affordable villa rentals at AED 153,000 annual rent.

- Affordable Off-Plan Properties: Popular affordable off-plan apartments included Reem Hills (AED 1.65 million), Royal Park (AED 934,000), and Al Reeman 1 (AED 793,000). Affordable off-plan villas in Al Reeman 2, Bloom Living, and Al Naseem Community ranged between AED 3.92 million and AED 4.1 million.

Rental Yields by Property Type & Key Areas

Abu Dhabi’s average gross rental yields stood at 5.39% in Q2 2025. Specific apartment rental yields in Q2 2025 vary by area and unit type:

- Al Reem Island: Studio 7.64%, 1-Bedroom 7.50%, 2-Bedroom 7.45%, 3-Bedroom 6.54%

- Saadiyat Island: 1-Bedroom 5.08%, 2-Bedroom 3.67%, 3-Bedroom 2.10%

- Al Raha Beach: 1-Bedroom 7.04%, 2-Bedroom 6.81%, 3-Bedroom 5.61%

- Yas Island: Studio 7.61%, 1-Bedroom 6.33%, 2-Bedroom 6.13%, 3-Bedroom 5.74%

Key Growth Drivers & Outlook

Abu Dhabi’s housing market shows strong momentum at the start of 2025, driven by rising interest in certain neighborhoods and signs of further price gains. Yas Island continues to be a standout due to its entertainment value, notably the announcement of Disneyland Abu Dhabi, which combines luxury living with leisure attractions like Ferrari World and Yas Marina Circuit. This mix makes the island highly attractive, especially given limited hotel availability, leading to strong rental returns, particularly in the short-term and holiday rental segments. Al Reem Island’s profile has been elevated by its inclusion under the Abu Dhabi Global Market’s authority, making it a top choice for investors of all nationalities due to its balance of city living and green space, attracting families and expatriates. The lack of municipal restrictions and strong rental returns further boost its desirability. Al Hudayriyat Island, a new development by Modon, blends scenic landscapes with city accessibility, appealing to buyers seeking luxury and practicality, with projects like Surf Abu Dhabi and Velodrome driving price growth. Al Raha Beach remains in demand due to its well-established waterfront location, robust infrastructure, and consistent demand from international buyers. Saadiyat Island is a prime choice for luxury buyers, blending high-end living with cultural destinations like the Louvre Abu Dhabi, attracting wealthy individuals from various countries and seen as ideal for long-term value growth.

5. Sharjah Property Market: Trends & Investment Landscape

Q1 2025 Transaction Volume & Value

Sharjah’s real estate market recorded significant growth in Q1 2025, with the total value of transactions reaching AED 13.2 billion, a 31.9% increase compared to AED 10 billion in Q1 2024. The number of executed transactions also rose by 4.8% to 24,597, up from 23,478 in the same period. This growth reflects increasing investor confidence in Sharjah’s stable and investor-friendly environment, supported by advanced infrastructure and a diverse range of investment opportunities.

A total of 8,123 sales transactions were recorded during the quarter, marking a 32.2% increase from Q1 2024. These transactions were spread across 169 areas, covering 46 million square feet and amounting to AED 10.7 billion Residential properties dominated the sales segment, accounting for 78.9% of transactions (2,894 deals). Industrial properties followed with 13% (477 transactions), commercial properties with 7.1% (259 transactions), and agricultural properties with 1% (39 transactions).

Property Type & Investor Demographics

Investors from 97 different nationalities participated in Sharjah’s real estate market during Q1 2025. Emiratis led with AED 5.2 billion (39.8% of total investments), followed by foreign investors contributing AED 4.5 billion (34%). The number of foreign investors increased by 25.3% year-on-year to 3,725, with 3,951 properties traded by non-UAE nationals, up 25.2%. This growth is largely attributed to legislative reforms permitting foreign ownership in designated areas of Sharjah. After Emiratis, Indian (796), Syrian (502), Egyptian (391), Iraqi (318), and Jordanian (303) investors were the top nationalities in terms of properties traded.

Rental & Sales Yields by Property Type & Key Areas

Sharjah’s rental apartment market experienced significant growth in 2024, with price increases ranging between 16% and 57%. Villa rentals in popular areas also saw an upswing, with prices rising by up to 25%.

For apartment sales in 2024, Al Nahda offered the highest projected rental yield of 7.50%. Other notable areas for apartment sales and their ROIs included Al Khan (4.47%) and Al Majaz (4.41%). In terms of rental prices for apartments in 2024, Al Nahda (Sharjah) saw average yearly rents of AED 25,000 for studios, AED 31,000 for 1-bedroom units, and AED 40,000 for 2-bedroom units. Muwaileh experienced significant increases in rental prices, with studios rising by 56.2%, 1-bedroom units by 47.5%, and 2-bedroom units by 36.3%.

For villas, the highest projected returns on investment (ROI) in Sharjah during 2024 were observed in Aljada (7.23%), Tilal City (5.52%), and Muwaileh (5.21%).

Impact of Legislative Reforms

Sharjah has seen a substantial increase in investment in its property market following government reforms that allowed all foreign nationals to own property in the emirate. This legislative framework, coupled with a diversified economy and stimulating investment climate, continues to consolidate Sharjah’s position as a thriving economic center. The distinguished performance of the emirate’s real estate reflects its competitiveness and attractiveness, drawing a wide range of investors and developers and enhancing opportunities for ownership, housing, and investment.

6. Key Drivers & Influencing Factors Across the UAE

The robust performance of the UAE property market in 2025 is attributable to a confluence of strategic drivers and influencing factors.

Population Growth & Demographics

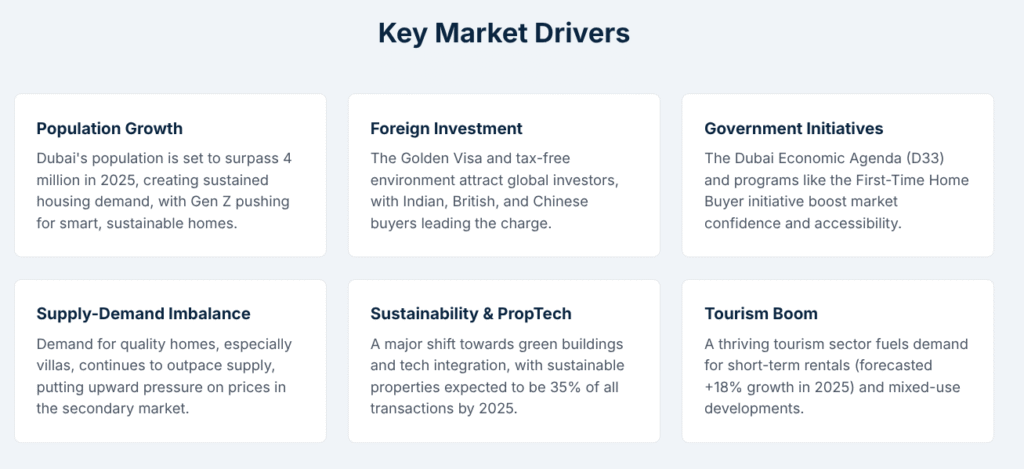

Dubai’s population reached approximately 3.91 million by Q1 2025 and is projected to surpass 4 million by Q3 2025, with long-term projections soaring to 4.6 million by 2030 and 5.8 million by 2040 under the D33 and Urban Master Plan frameworks. This rapid population growth, driven by both expatriates and local residents seeking long-term housing solutions, underpins a sustained demand for residential properties across the UAE. The influx of over 100,000 individuals benefiting from the Golden Visa program, many of whom are investing heavily in real estate, further fuels this demand.

A notable shift in buyer demographics includes the increasing entry of Generation Z (born 1997-2012) into the property market. This technologically astute and sustainability-focused cohort is reshaping demand, favoring properties with smart home adaptations, high-specification security systems, remote lighting and temperature control, and eco-friendly features. Developers are responding, with the percentage of new properties in Dubai incorporating smart technology expected to rise to 60% by the end of 2025.

Foreign Investment Inflows

The UAE real estate market remains highly attractive to global investors, with strong foreign investment from Indian, British, Chinese, Saudi Arabian, and Russian buyers. Indian investors continue to be the largest foreign buyer group in Dubai, increasing their market share from 21% in 2024 to 22% in 2025, driven by geographical proximity, a tax-free environment, and currency depreciation benefits against the dollar-pegged dirham. British investors maintain a strong presence, with their market share rising to 17% in 2025, often acquiring properties for rental income due to attractive yields compared to UK market conditions. Chinese investment has grown to 14% in 2025, bolstered by the Belt and Road Initiative and the Golden Visa program. Saudi Arabian nationals now hold an 11% share, favoring high-end residential properties due to cultural ties and ease of travel. Russian investors, with a 9% market share, continue to show strong demand for luxury properties, viewing Dubai as a safe-haven investment destination amidst geopolitical uncertainties.

Government Policies & Initiatives

Strategic government initiatives play a pivotal role in shaping the market. Investor-friendly reforms, tax incentives, and streamlined processes continue to attract significant foreign direct investment. The Dubai Economic Agenda D33 aims to position the emirate among the top three urban economies, with the Dubai Real Estate Strategy 2033 focusing on doubling the sector’s contribution to GDP and fostering an integrated ecosystem rooted in innovation and technology.

Recent initiatives include the Dubai First-Time Home Buyer Program, launched in July 2025, offering preferential terms on properties up to AED 5 million for UAE residents who have never owned a freehold home. This program provides priority access to new project launches, flexible payment plans, zero-interest registration fees, and attractive financing options.23 Furthermore, the UAE has strengthened its Anti-Money Laundering (AML) compliance framework, requiring enhanced due diligence for high-risk buyers and full verification of buyer identities and source of funds, ensuring transparency and security in transactions, including those involving cryptocurrency.

Supply and Demand Dynamics

While demand for residential properties surges, supply continues to lag in many segments, creating significant opportunities for investors. Over 25,000 new apartment units and nearly 6,600 townhouses and villa units were registered in Q1 2025, with a total of 81,084 units expected by year-end. However, a forecasted 41% year-on-year increase in residential handovers in 2025 may affect market dynamics. There are warnings from credit-rating agencies, such as Fitch, projecting a potential double-digit price decline of up to 15% in late 2025 and into 2026, as over 210,000 units enter the pipeline—nearly double the supply of the prior three years—risking a material supply-demand imbalance. This looming adjustment, however, also represents a strategic entry point for first-time buyers.

Sustainability & Smart Developments

Sustainability is becoming a key driver in the real estate market. By 2025, 35% of new office spaces in Dubai will be LEED-certified, up from 25% in 2023, reflecting the city’s push for eco-friendly urban growth. PropTech is revolutionizing the market, with IoT-enabled homes, AI-powered security, and blockchain for seamless transactions. Sustainable properties are expected to account for 35% of total transactions by 2025. This trend is particularly influenced by younger buyers, with 72% of Gen Z reporting altered behavior to minimize environmental impact. Demand for green-certified developments featuring energy-efficient designs, EV charging stations, and smart lighting is increasing.

Tourism & Hospitality Sector Growth

Dubai’s booming tourism sector significantly contributes to real estate demand. Short-term rental demand is expected to grow by 18% in 2025. The growth of the hospitality industry, with hotel revenues of AED 33.5 billion and among the highest occupancy levels globally, enhances demand for mixed-use developments. This convergence of tourism, hospitality, and real estate strengthens the global investment attractiveness of the UAE.

Mortgage Market & Interest Rates

The UAE witnessed strong mortgage activity in Q1 2025, driven by sustained demand and investor confidence. Dubai alone recorded 11,014 mortgage transactions with a total value of AED 41.1 billion. Abu Dhabi reported AED 9.0 billion in mortgage transactions across 2,846 deals during Q1 2025. This growth reflects a maturing market, supported by favorable lending conditions and ongoing demand in both ready and off-plan property segments. However, rising mortgage rates, with the 12-month EIBOR reaching 5.306% in June 2024 and retail mortgage rates for expatriates at 6.65%, are compressing affordability for mid-income buyers, particularly for those relying on 85% loan-to-value structures. Despite this, national interest rates have gradually decreased over the past 12 months, following Federal Reserve changes, making mortgages more affordable and increasing consumer borrowing capacity.

7. Conclusions

The UAE property market in 2025 is characterized by robust growth and dynamic shifts, solidifying its position as a leading global investment destination. The market’s strength is rooted in the UAE’s diversified economy, particularly the strong performance of its non-oil private sector, which provides a fundamental buffer against global economic uncertainties. This economic resilience enhances investor confidence, making the market less susceptible to external shocks.

Dubai continues to be a powerhouse, with record-breaking transaction volumes and values, notably driven by the secondary market and an exceptional surge in the ultra-luxury segment. This indicates a “flight to quality” among buyers, who are increasingly prioritizing ready, high-quality properties, especially villas and townhouses, in established communities. The remarkable growth in the luxury segment is not merely a niche trend but a significant catalyst for overall market value, reflecting robust confidence from high-net-worth individuals in Dubai as a long-term investment and lifestyle hub. While off-plan properties remain attractive for future capital gains, the immediate market momentum lies with existing, desirable assets.

Abu Dhabi also demonstrates steady and broad-based growth across all segments, with specific luxury and affordable hotspots showing strong performance, driven by strategic developments and improved infrastructure. Sharjah’s market is experiencing significant expansion, largely propelled by recent legislative reforms that have opened up foreign ownership, attracting a diverse international investor base.

Despite the overall positive outlook, the challenge of affordability persists, particularly for mid-income earners, as the supply of truly accessible housing struggles to keep pace with demand. This imbalance, coupled with rising mortgage rates, presents a complex landscape that requires ongoing governmental and developmental attention to ensure a balanced and inclusive market.

Key drivers such as sustained population growth, attractive Golden Visa programs, and proactive government policies continue to fuel demand and investment inflows from a diverse range of international buyers. The increasing focus on sustainability and the integration of PropTech are also reshaping the market, aligning with evolving buyer preferences, especially among younger demographics. The thriving tourism and hospitality sectors further underpin demand for various property types, from short-term rentals to mixed-use developments.

In essence, the UAE property market is demonstrating a sophisticated evolution. It is a market that is not only expanding in volume but also maturing in its dynamics, with distinct trends across emirates and price bands. This necessitates a granular understanding for any stakeholder seeking to navigate its opportunities effectively.